40 Year Fixed Rate Mortgage?

In a surprise move a specialist mortgage company in the UK has just launched a 40-year fixed rate mortgage deal!

This means that borrowers will pay the same instalment rate for up to four decades. The rate will not change even if the Bank of England increases or decreases their base interest rates.

It unheard of in the UK to find a fixed rate mortgage that will span the entire term which is typically 25 years. Most fixed rate mortgages last for 2 – 5 years.

Interest rates hit a record low in 2021 at 0.1% but the BoE is predicted to increase the rates in the near future.

It sounds amazing to secure a long term fixed-rate mortgage which allows you to reap the benefits of record low interest rates for the long term but what could be the downfalls of such a deal?

The main disadvantage of agreeing to a long term, fixed rate deal is that you will incur large fees if you want to pay off the mortgage early. If you want to leave the mortgage within the first 15 years you will incur a fee of 7% of the remaining balance.

You will be able to port the mortgage to another property & there are no penalties for sell or if the mortgage holder is impacted by critical illness or dies.

The interest rate for this fixed rate for 40 years will start at 3.34% & deposits will be 40% or 50%.

If you opt for a 40% deposit you will be borrowing 60% of the house value. You will also need to pay an arrangement fee of £1,499.

People with only a 5% deposit will pay a higher rate of 4.16% & pay the same arrangement fee.

Rates start at just 2.83% for those people wanting to fix shorter term deals of between 11 and 15 years.

BUT…

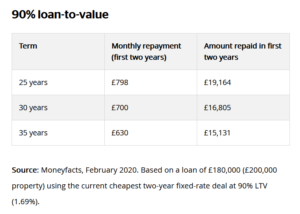

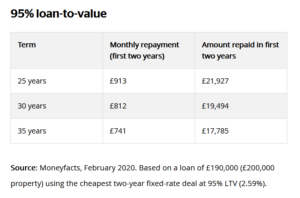

A longer term certainly results in lower monthly costs & we’ve found that you can save as much as £100 a month by choosing a 30-year term rather than a 25-year term.

The tables below show that at 90% loan-to-value (LTV), adding an extra five years brings the payment down to £98 a month, or £101 at 95% LTV. Stretching the term to 35 years saves a further £70 a month taking the total saving to around £170.

Although it can be more affordable in the short term to take out a longer mortgage, it will take you longer to pay off the loan and you will pay more in interest. On average for every five years you add on to the mortgage term, you will pay off around £2,000 less during the initial two-year period.

Taking out a longer-term mortgage might be the only way, for some borrowers, to be able to afford a property. The best ideas with mortgages is to take advantage of deals when they are available & suit you best.

Currently, mortgage rates are very low, and most lenders allow overpayments of up to 10% of the balance each year. If you can put some extra money towards your loan (either monthly or on an ad-hoc basis) it’s possible to pay off your mortgage much earlier and make big savings along the way.

As an example, if you borrowed £200,000 over 30 years (at a rate of 3%) & paid an extra £50 a month you would cut more than two and a half years off your term and save £10,000 in interest.

You can find out how much you can save or spend by playing with this mortgage overpayment calculator

Then again if you can afford larger repayments, it would be well worth considering a 10 or 15 year mortgage.

You can play with the sums on this calculator

Do let me know what you think…

p.s. I am not endorsing the calculator websites I randomly found online they are just illustrations to help you… I am sure you will be able to find similar calculators for your country & currency